“No email, no app notification, nothing,” Mishra recalled. “I had paid ₹20,000 upfront for an annual plan for me and my partner.” He says Cult.fit was unresponsive when he sought help and that pushed him to air his frustration on microblogging platform X.

Determined to squeeze out some value for his money, Mishra shifted to Cult.fit’s Juhu centre, a few kilometers away. Six months later, that one shut too. The next option? Lokhandwala, over 7km away. “Some days, the auto fare was more than what I was paying per class,” he said. But even that centre closed its doors in April this year.

Mishra’s story isn’t an outlier. Social media is awash with similar complaints—of customers locked into year-long memberships only to find their neighbourhood centres shuttered. While gym closures aren’t rare in the fitness industry, Cult.fit’s recent wave of shutdowns has raised eyebrows.

View Full Image

However, the company—officially known as Curefit Healthcare Pvt. Ltd—maintains it’s a routine operational matter. “There will always be the bottom 5-6% that don’t pan out,” chief executive officer (CEO) Naresh Krishnaswamy told Mint. “That churn is what we do every year.”

He insists that proper communication is ensured during centre closures, with timely updates, nearby alternatives and refund or transfer options.

But with multiple centres closing across cities, the churn raises questions on the scalability of Cult.fit’s model. Rivals cite their own record to question the closures. “I will not say that Anytime Fitness has not shut gyms in the past, but of about 175 gyms, we have shut down 7-8 in the last 13 years,” said Vikas Jain, the chain’s managing director. “But yes, in other brands or other standalone gyms, there are a lot of closures, which is not good. As we are an industry where people pay full amounts in advance, when you shut down, the trust goes down.”

Rapid rise

Cult.fit was founded by former Flipkart colleagues Ankit Nagori and Mukesh Bansal in 2016. Within a few years, they turned it into India’s biggest organized fitness chain, backed by funding from marquee names such as Zomato, Tata Capital, HDFC Bank and Kotak Mahindra Bank. That war chest helped put Cult.fit’s growth on steroids, as it took the inorganic path to set up a network of 700 centres across major cities.

View Full Image

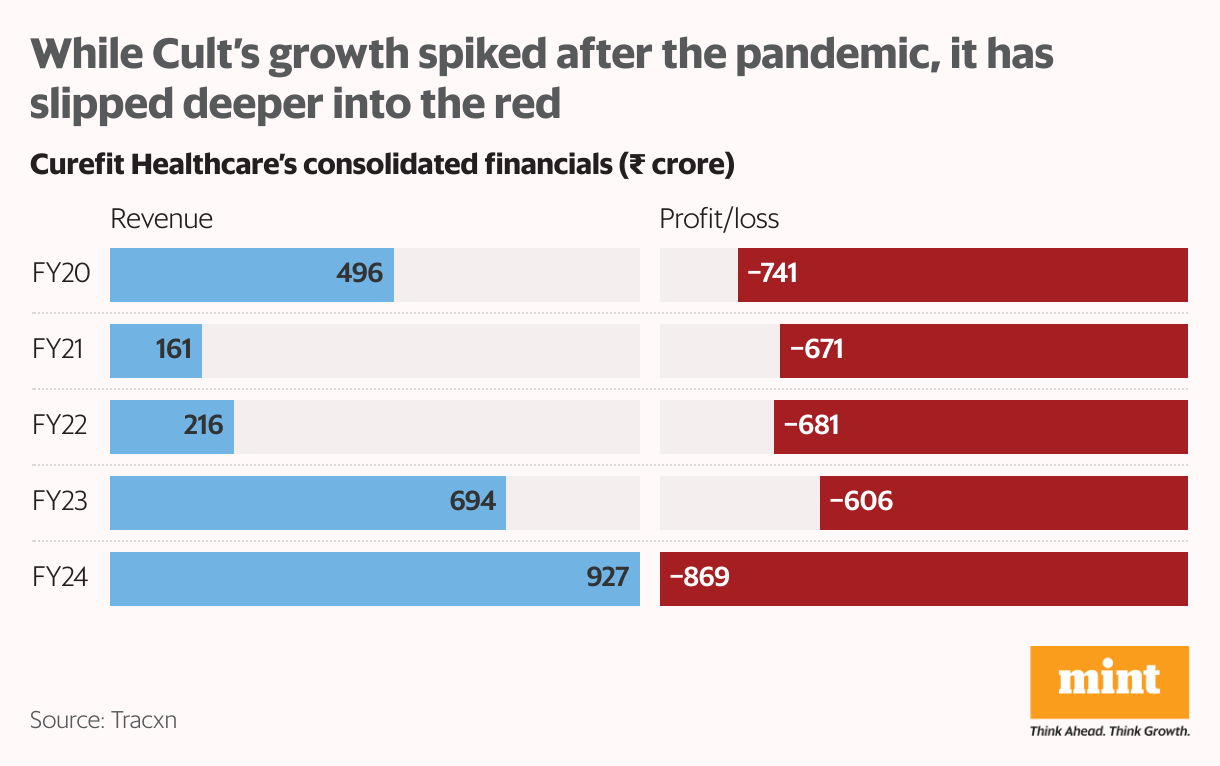

But after bulking up at a rapid pace, the company’s growth has begun to lose pace. Cult.fit has slipped deeper into the red, reporting losses of around ₹869 crore in 2023-24 against revenue of ₹927 crore.

Cult.fit claims to have an active subscriber base of about a million. Services, including gyms, group classes and Cult Play contribute two-thirds of the business, while sports apparel and equipment account for the other one-third.

Balancing pricing to improve margins without stalling growth will be a key challenge in the company’s core fitness centre business, especially as the broader market remains limited. At the same time, it is still burning cash in its sportswear and equipment vertical, where gaining ground against established players has proven difficult.

According to media reports, the company is now eyeing an initial public offering (IPO). This will be a milestone if it happens, as it will be India’s first serious fitness IPO attempt since the last one, by Talwalkars, a dominant gym chain that eventually crumbled under the weight of debt and unchecked expansion.

Krishnaswamy, a long-time insider who took over the CEO role in October 2023, having previously served as Cult.fit’s head of finance for over three years and then leading its growth and business divisions, isn’t worried about going the Talwalkars way. Indeed, despite Cult.fit’s heavy losses, he claims profitability is just around the corner. If that happens, it will be a turning point. But from a long-term perspective, can the startup show endurance and scale up sustainably?

View Full Image

Premium fitness centres

Nagori and Bansal started the company in 2016 as Curefit, with the intent of creating a holistic wellness platform covering physical and mental health, food and nutrition. Many earlier startups focused solely on the physical side of fitness, a model that didn’t quite click, prompting the founders to build a broader preventive health platform. Bengaluru, Cult.fit’s biggest market, is where operations kicked off.

Curefit began by acquiring a controlling stake in Cult, a startup founded by Rishabh Telang, which differentiated itself from traditional gyms by offering fitness training in the form of martial arts, kickboxing and other activities. Interestingly, Bansal, formerly fashion etailer Myntra’s CEO, was a user of the original Cult gym and had invested his own money in it. Cult operated two fitness centres in Bengaluru when it was acquired. It expanded to Delhi, Hyderabad and Mumbai, and eventually to Chennai, Jaipur and Pune, among other cities.

The holistic wellness idea gained traction, with the company raising over $650 million from the investors mentioned above as well as others such as Accel, Temasek and Chiratae Ventures. Curefit rebranded to Cult.fit in 2021 to reflect the company’s focus on its flagship fitness vertical. Eatfit, the food vertical, which was severely impacted during the covid-19 pandemic with subscriptions declining, was spun off as a separate entity.

Over the years, the company has managed to become the largest branded fitness chain in the country—while its 700 centres are spread across 40 cities, about 80% are in Bengaluru, Delhi, Hyderabad and Mumbai, according to Krishnaswamy.

Cult.fit built that huge footprint through a rapidfire acquisition strategy, and has snapped up over 20 startups since inception. In 2021 alone, it acquired seven companies. The most prominent was India operations of the Gold’s Gym, which gave it a massive boost in reach, adding over 140 centres across 90 cities, including deep access into tier-II and III markets.

The company’s competitors in India include global fitness chains Anytime Fitness and Snap Fitness. In the last few years, it has been trying to build a brand in the products business, selling apparel, shoes and sports equipment.

A typical Cult.fit fitness subscription costs ₹14,000-16,000 annually. For context, Indians on an average spend between ₹4,000 and ₹10,000 annually on preventive healthcare, which includes exercise, healthy nutrition, health insurance, early diagnosis and health tracking, Nikhil Kamath, co-founder at Zerodha, had noted in an X post in February. Moreover, 35% of the richest Indians account for 98% of preventive healthcare spending, according to the post.

Chasing numbers

Cult.fit reported a 33.5% rise in revenue in 2023-24 to ₹927 crore, even as its losses widened 43% to ₹869 crore, according to financials sourced from Tracxn. The losses were driven by goodwill impairment costs. A year earlier, the company had recorded 221% growth in its top line, albeit on a smaller base.

There’s a downturn in performance in FY24, but Krishnaswamy believes Cult.fit will comfortably hit 30% year-on-year growth over the next few years. “The growth in 2022-23 was on the back of a lower base the year before (the pandemic year). The growth rate has normalized in 2023-24. I frankly don’t feel any pressure to grow faster,” he said, adding that the industry is growing at about 15%.

While the CEO believes that there’s no saturation, multiple current and former executives, as well as industry watchers told Mint that penetrating existing cities further has been tough. As compared to about 21.2% of the adult population with a gym membership in the US, only 0.2% are gym members in India.

A rising urban middle class and disposable incomes are all factors that point in a positive direction, but the revolution in fitness awareness is happening only in a limited set of customers in small pockets. “While there’s huge scope, the growth’s happening very slowly,” an industry executive, who didn’t want to be identified, told Mint.

The capex-heavy fitness centre business in India faces two persistent, structural challenges: first, a chronic underutilization of assets with only 30% of gym capacity being used; and second, poor renewal rates, often below 25%, according to Akshay Verma, co-founder of FITPASS, a platform offering users access to various gyms and workout classes.

“These stem from a mix of issues: high upfront membership costs, consumers wanting variety in workout formats, high trainer attrition and a general sense of not receiving enough value from the service experience,” Verma added. “Over $3.4 billion in fitness infrastructure lies idle every year. The problem is not a lack of supply—infrastructure is ready and waiting. The real question is why are people not gushing through the gates?”

Krishnaswamy, however, is optimistic about Cult.fit’s prospects. “The fitness services business or gym business is already cash flow-positive and we are about a quarter away from becoming Ebitda positive. We continue to invest in the product business because it’s a growth category for us and we are still a relatively small player in a large market,” he said.

“Towards the last two quarters of this year, the combined business will be Ebitda-profitable with the services business obviously being heavily profitable,” Krishnaswamy added.

Ebitda is short for earnings before interest, taxes, depreciation and amortization.

Vertical limit

Apparel, shoes and sports equipment, which Cult.fit refers to as the products vertical, are seeing a big push. The company expects this line of business to increase its contribution from the current 30% or so to about 50% in the next two-three years and surpass the core business eventually. Krishnaswamy believes there is a gap the company is tapping between entry-level player Decathlon and high-end brand Nike or Puma.

“They started this because in the gym business you won’t get the valuation for an IPO. But they really have not been able to translate their brand position in the gym business into sales of apparel or footwear,” said a former company executive who didn’t want to be identified.

Cult.fit also expanded offline in 2023, which, according to current employees and industry executives, is going well. Continuing to improve products and making offline work will be key determinants for the company’s future success, said Krishnaswamy.

While products is a big category, the major hurdle is competition, with many brands operating in the space, Decathlon being the biggest one. The company needs to spend heavily if it is to take on the French giant.

But Cult.fit is stuck, say industry insiders, as it cannot spend much because it has to become profitable. At the same time, the revenue numbers need to rise for it to get a good valuation.

Another bet by the company, Cult Play, has not worked out despite multiple attempts, according to sources. Play essentially included badminton and swimming courts under Cult.fit’s brand for users to learn the sports. The CEO said it is a small category but it is building the vertical steadily as it is important from a long-term perspective.

The road ahead

According to media reports, Cult.fit is planning to raise ₹2,500 crore through an IPO at a proposed valuation of $2 billion. Analysts, however, are worried about the startup’s profitability challenges.

“Despite brand visibility and the involvement of big names, the company’s financial conditions do not justify a confident entry. Investors should adopt a cautious approach,” V.L.A. Ambala, a Securities and Exchange Board of India-registered research analyst, said.

To be fair, Cult.fit built India’s biggest fitness chain and made premium workouts mainstream in urban India. But the real challenge is getting more people through the door and keeping the growth engine running.

View Full Image

Krishnaswamy, meanwhile, has his task cut out, with the two founders now focused on other ventures—Nagori is leading Curefoods, which spun off from Curefit’s food business in 2020, and Bansal is focusing on new startups he has cofounded, such as omnichannel fashion brand Lyskraft, and agentic artificial intelligence company Nurix AI.

In its core business, Cult.fit is ahead of the pack, but as Krishnaswamy admitted, “What we are fighting is the resistance of people to join fitness programmes.” Over the next three-five years, he added, the company will look to expand the market.

But for that to happen, Indians will need to get off the couch.